This article is from HBAV's historical archive. Some formatting may differ from current articles.

By Jeff Kelley for HBAV.com

While interest rates are expected to fall, and inflation is cooling, it is the housing industry’s regulatory burdens, fees, and policy-driven delays that will continue to create higher costs of living — and borrowing — for Americans.

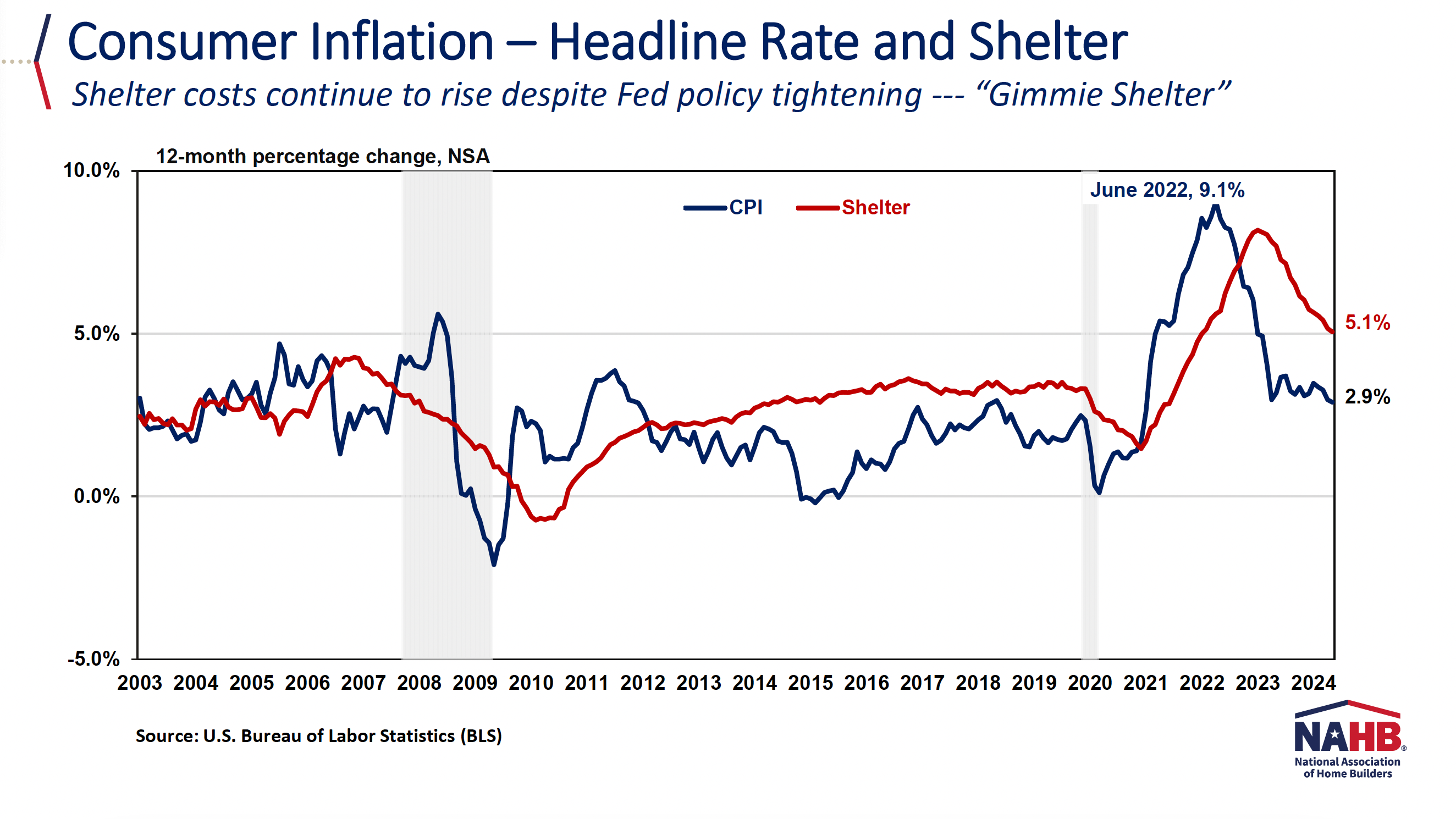

That was the message delivered this month to Virginia home builders by Robert Dietz, Ph.D., chief economist of the National Association of Home Builders. Currently, inflation sits around 3%, above the Federal Reserve’s “stable” target of a 2% annual price change index for personal goods and services. When households and businesses expect inflation to remain low and stable at 2%, they can make sound decisions regarding saving, borrowing, and investment, which contributes to a well-functioning economy.

But reaching 2% will be difficult for one singular reason: Shelter inflation, which rests at about 5%, Dietz noted. Housing costs have frozen overall inflation at about 3%.

“The housing deficit has kept housing costs rising [at] almost twice as fast as overall inflation, and that’s not something the Federal Reserve can solve. The only way to tame that last leg of the inflation fight is to build more attainable housing for sale and for rent,” Dietz told builders and suppliers in the event hosted by the Home Builders Association of Virginia.

If shelter inflation came down, he said, “it would be mission accomplished.”

In general, Dietz was cautiously optimistic on the housing market, emphasizing the importance of addressing labor shortages, regulatory burdens, and economic factors to ensure sustained growth. Beyond inflation, he covered a broad swath of economic indicators and offered a glimpse at where the American economy may be headed.

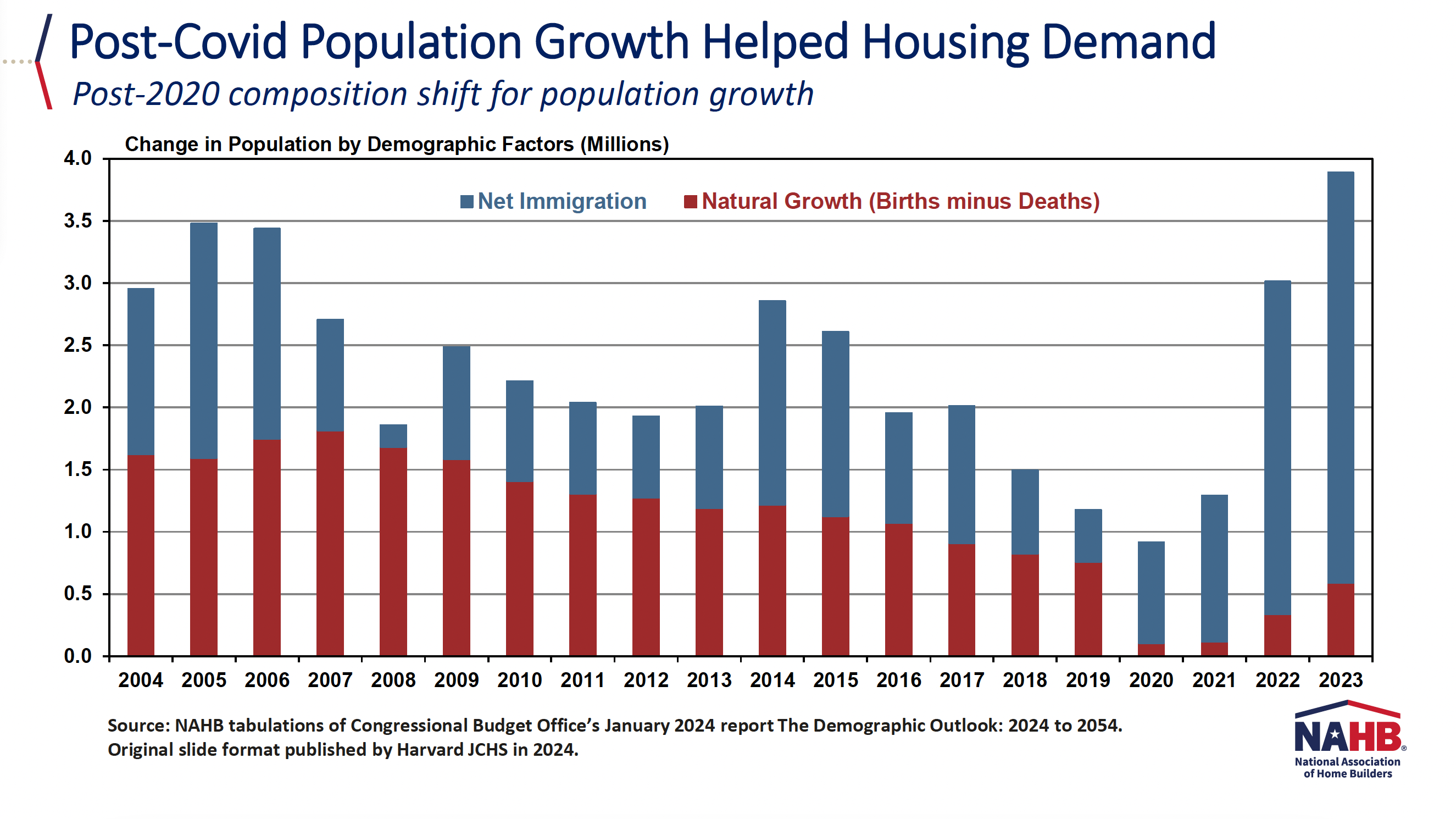

Population Growth led by immigration

Natural birth rates are down considerably and have been falling steadily since the 2008 recession, but the U.S. population is soaring due to net immigration.

“Obviously that’s going to be an election issue in terms of border control and immigration status, but from an economic growth status, it means there are more people here spending more money,” Dietz said. “Some of that money is government support, but that spending power has also supported the economy in the short run.”

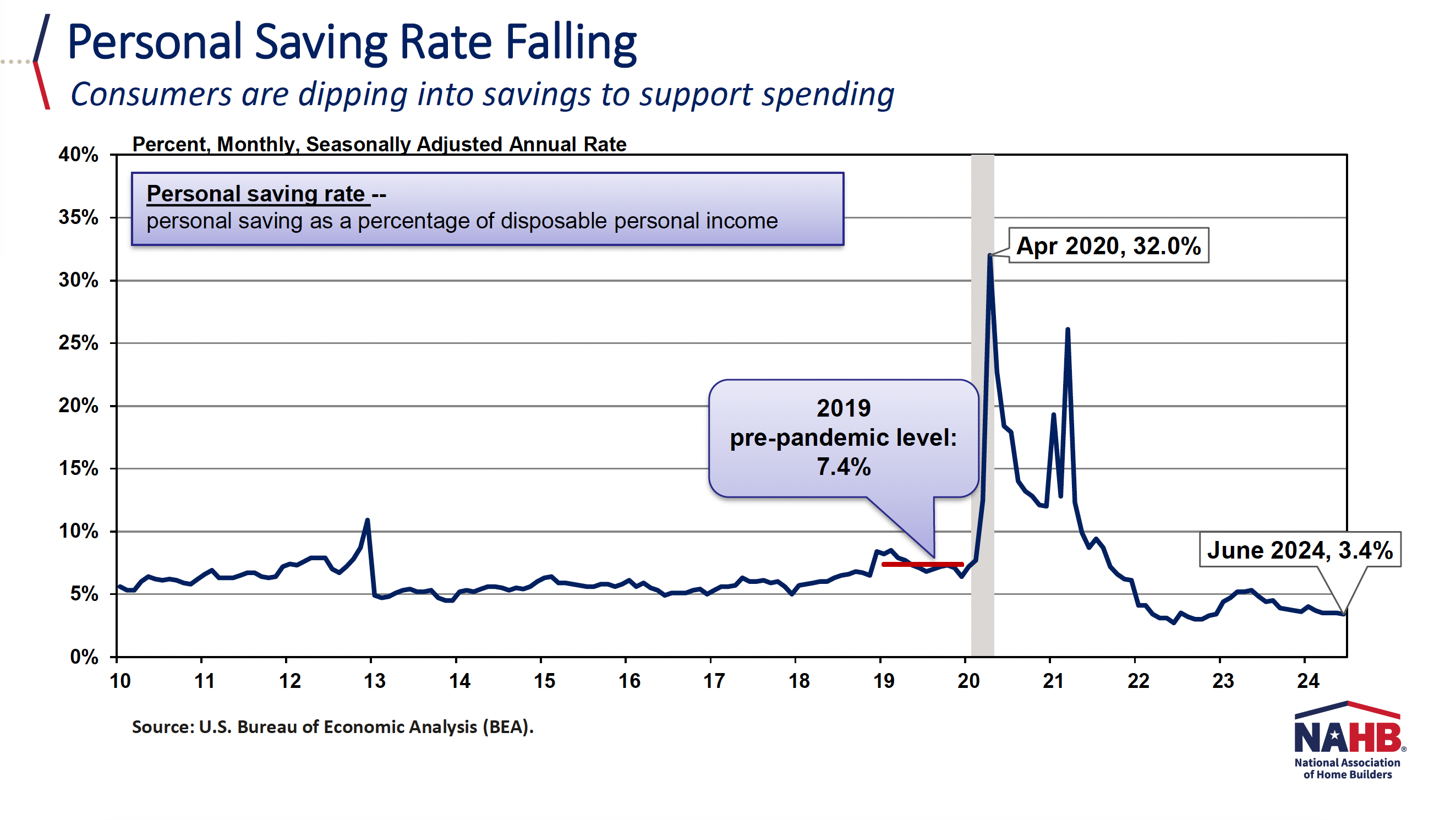

Personal savings are down

The personal savings rate has significantly decreased from over 7% in 2019 to 3.4% in June 2024. This decline suggests that future consumer spending, which often relies on savings, is likely to weaken.

This trend aligns with recent reports from popular consumer companies like McDonald’s and Starbucks, indicating a slowdown in spending.

Jobs and unemployment

The labor market is showing signs of slowing, consistent with the broader economic forecast.

- The unemployment rate is approaching 5% and is expected to rise further in the coming quarter; the rate is often a lagging indicator of economic weakness.

- The job openings rate, which peaked at 12 million in early 2022, is down to about 8.2 million due to higher rates. This reduction in job openings suggests a cooling labor market and may prompt the Fed to consider cutting interest rates soon.

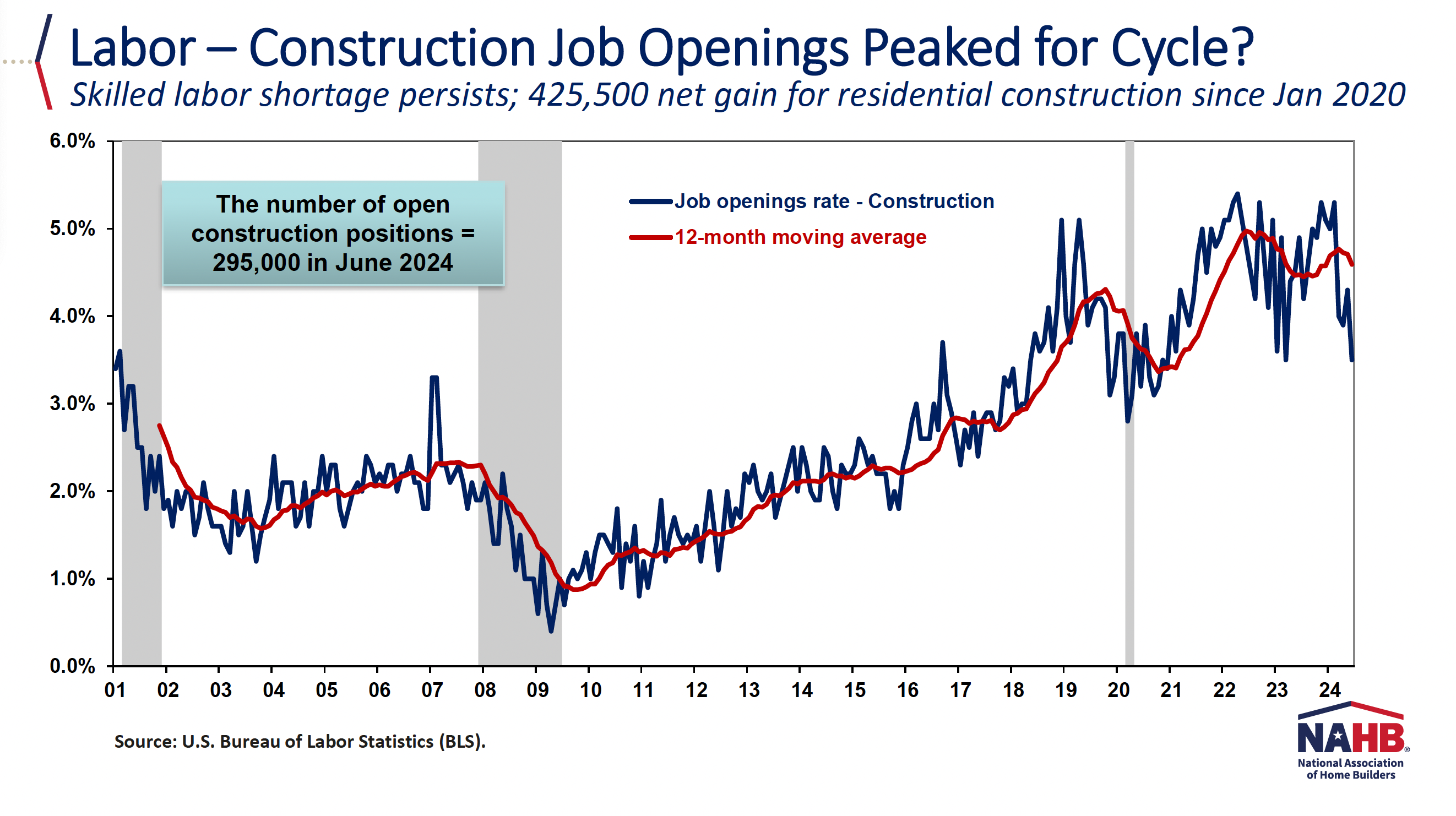

- The skilled labor shortage in construction has seen fluctuations but is expected to worsen again by 2025-2026. Efforts to develop the skilled labor force are crucial for the industry’s future.

Since the pandemic, the U.S. has seen a 4% increase in jobs compared to pre-pandemic levels, with similar recovery trends in Virginia. Some states, like Idaho and Utah, have experienced even higher job growth.

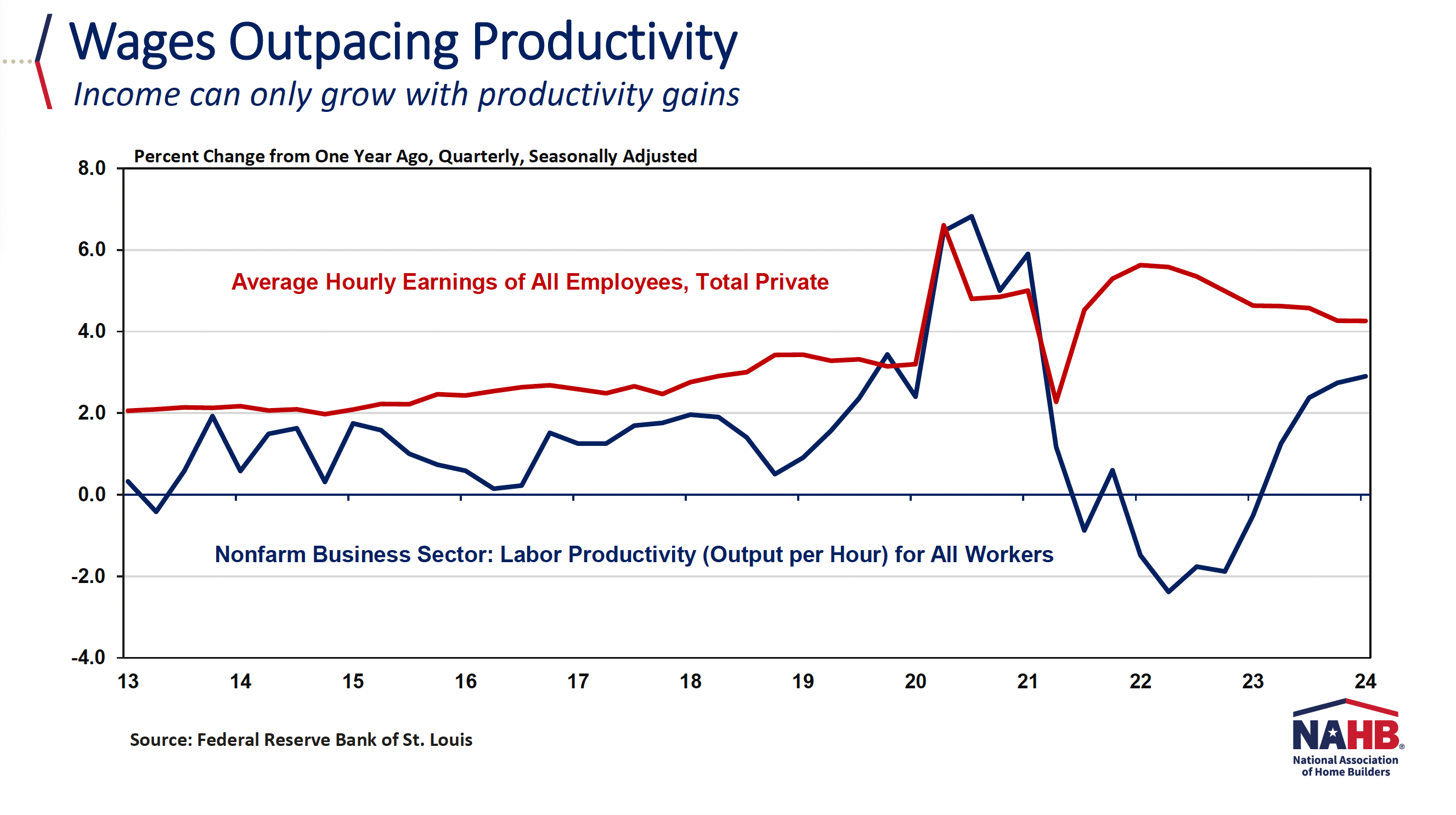

Wages and Productivity

Wage growth has outpaced productivity growth since 2021, contributing to inflation. However, recent data shows wages and productivity growth are converging, which is a positive sign and may further support the Fed’s rate cuts.

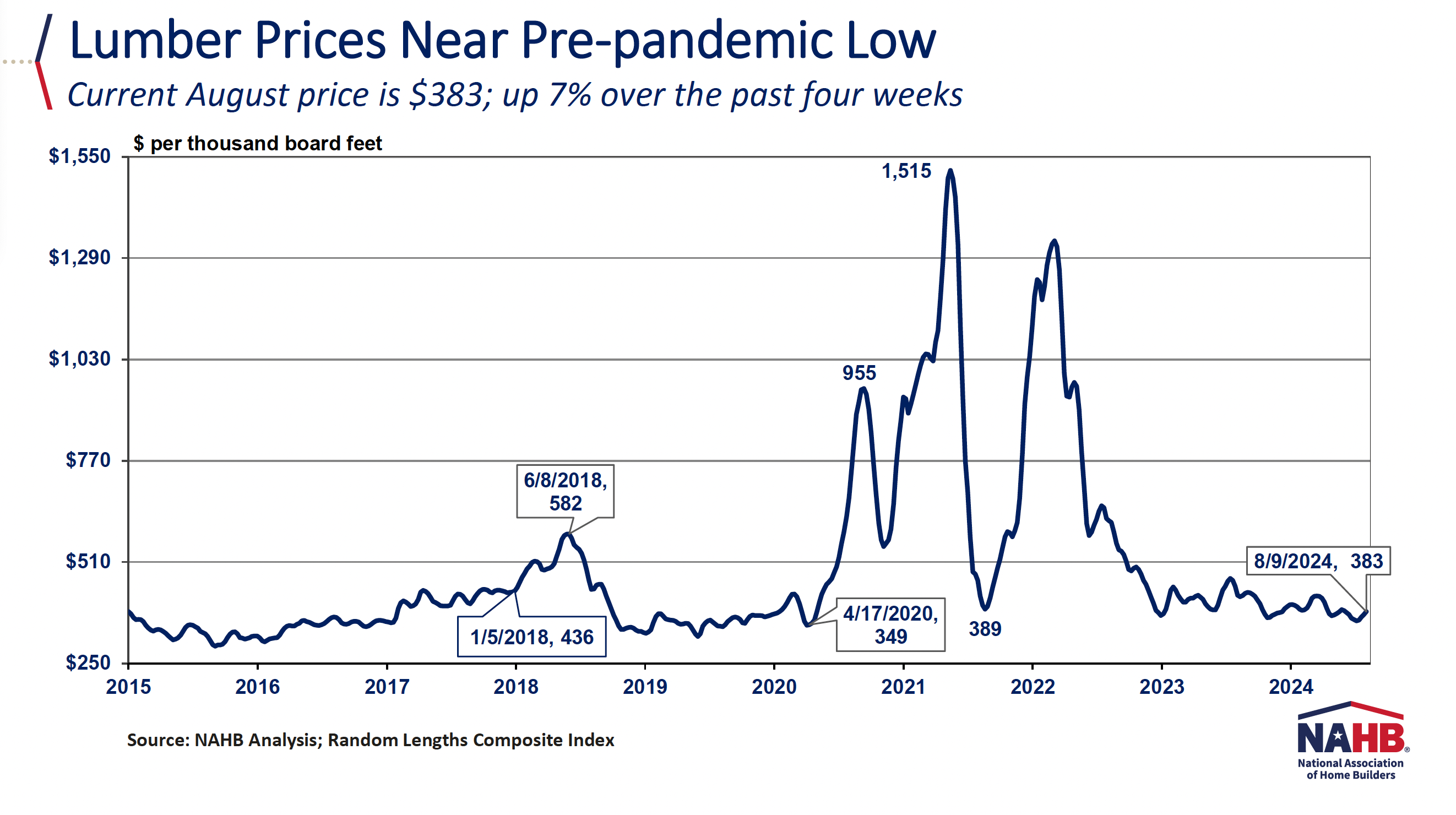

Lumber Prices and Tariffs

Lumber prices have been relatively low but are expected to rise due to a recent increase in tariffs on Canadian softwood lumber. This is reminiscent of 2018, when higher tariffs led to a significant price spike.

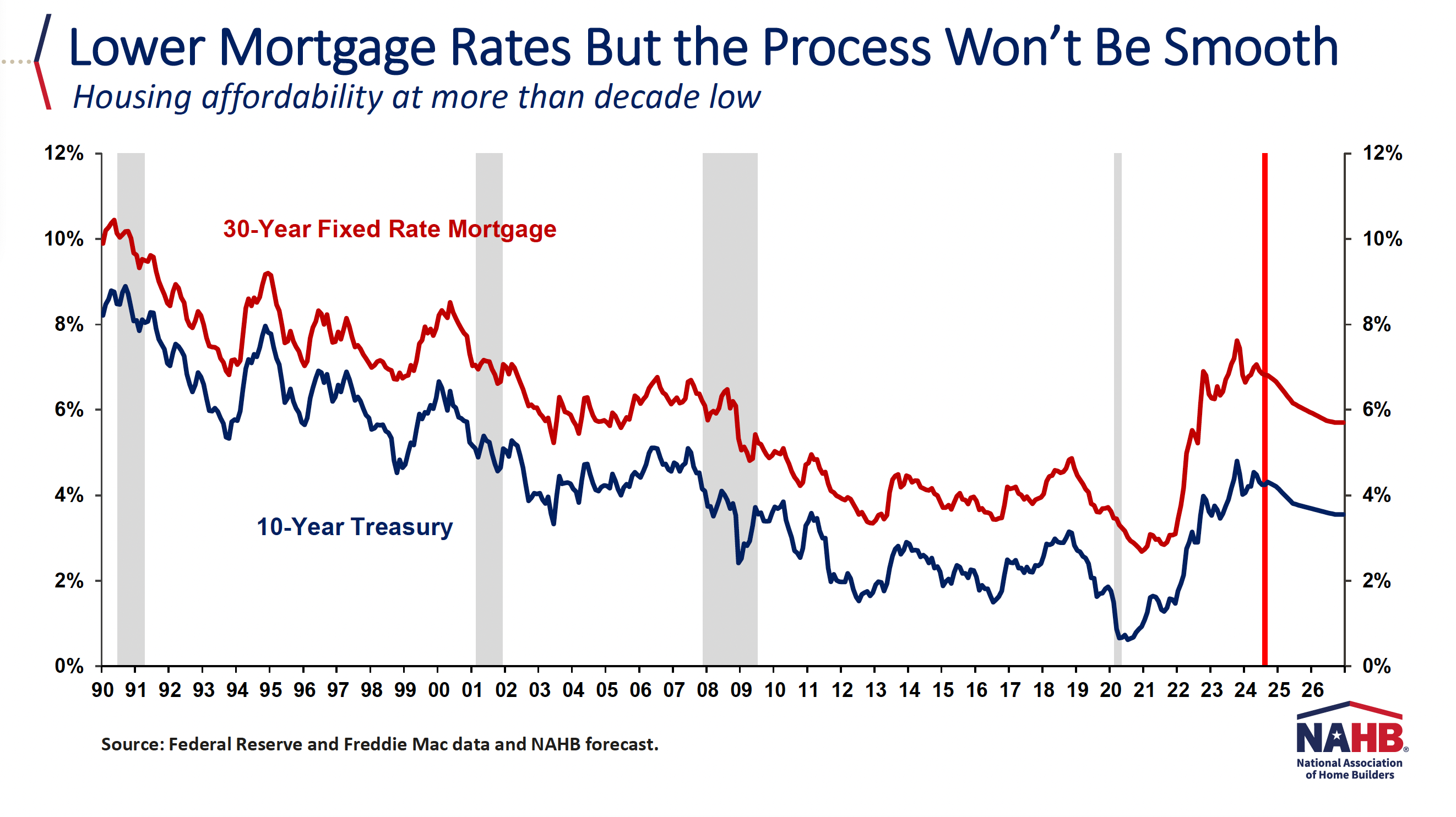

Loan Conditions

Construction loan rates are currently high (12-15%) but are expected to decrease as the Fed cuts rates, benefiting smaller builders.

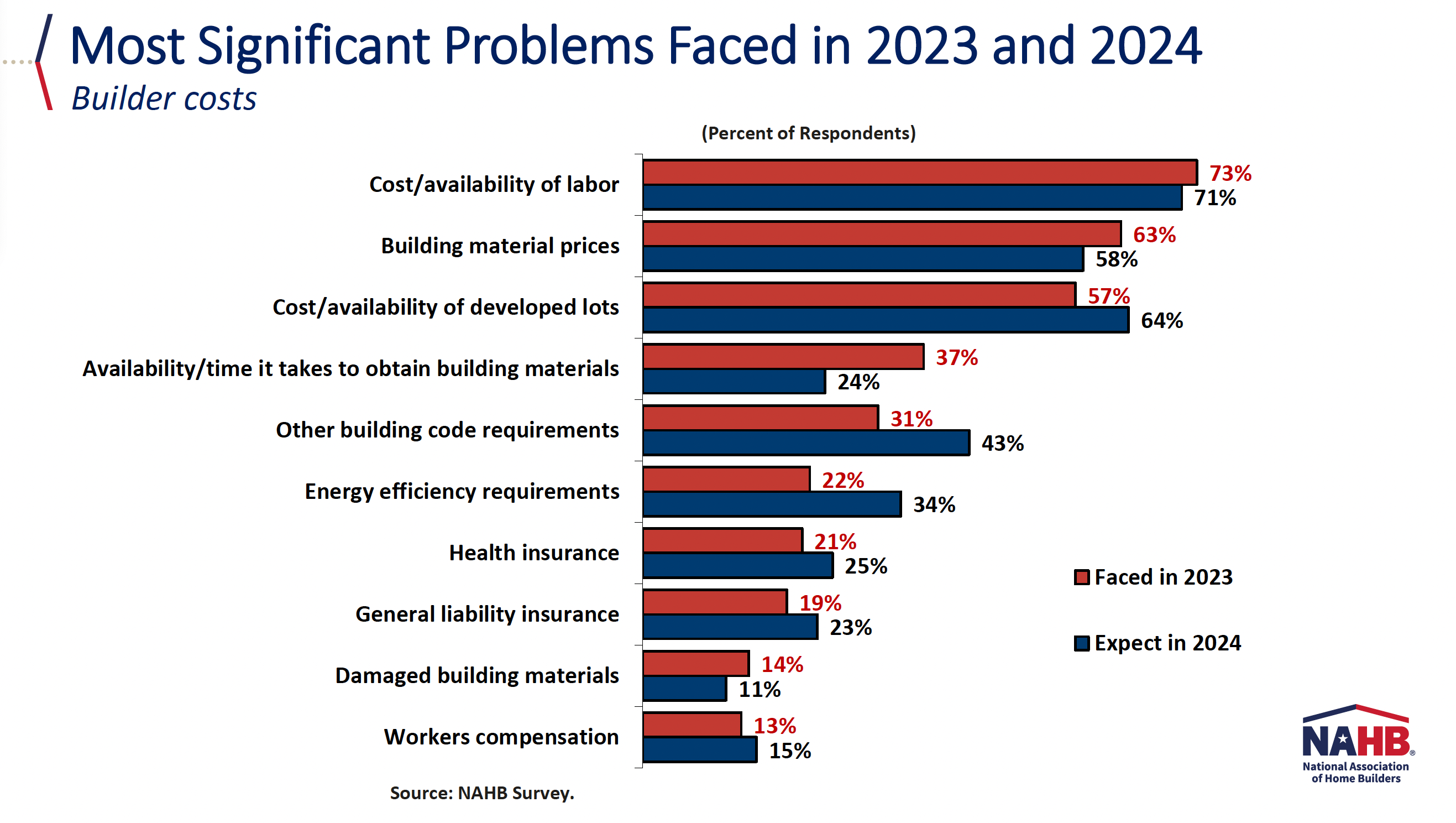

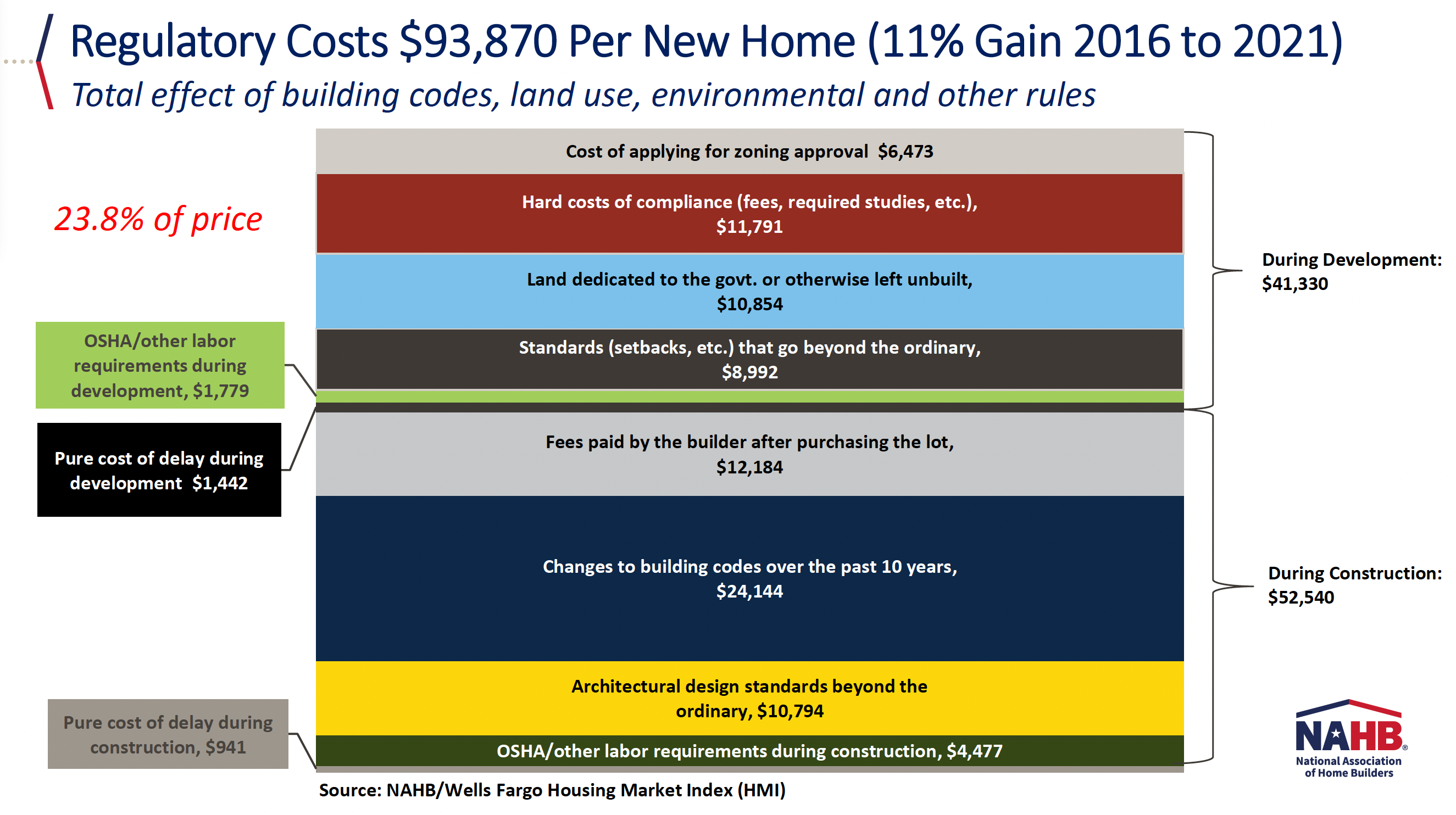

Regulatory Costs

Regulatory costs account for about 25% of a new single-family home’s price.

“Inefficient costs get built into the system,” he said, noting his message to policymakers: “If you’re looking for ways to allow builders to build that more entry-level home, more affordable, attainable housing, reduce these costs. There’s a large number of [regulations]. Pick a couple and reduce them and bend the cost curve in the right direction.”

Housing Market Trends

- Inventory: Housing inventory remains low, despite new home inventory levels being above nine months.

- Single-Family Home Construction: After declines in 2022 and 2023, single-family home construction is expected to grow by 6% in 2024, with continued growth into 2027 to address the housing deficit.

- Custom Homes: The segment remains stable at about 20% of the market, but focusing on larger, more expensive homes.

- Home Size: New home sizes have been declining for a decade but are expected to increase again by 2026 as interest rates drop.

- Multifamily Construction: The anticipated decline in apartment construction is underway, with a 30% drop expected this year. However, the market is expected to stabilize and grow by 2026.

Demographics and Future Challenges

The current demographic trends are favorable for housing, with a large millennial population entering the homebuying market. However, the declining fertility rate will lead to fewer potential homebuyers in the future, particularly affecting rental demand and first-time homebuyers by the 2030s.